Financial Planning for Salons on a Budget

Financial planning isn’t a skill that comes naturally to most salon and spa owners. Finances can be incredibly stressful, especially in the early days when you may be on a tight budget.

Owning a successful beauty salon or spa requires a blend of skill sets. You have to be talented at your trade and ready to hustle for clients. But you also need a solid head for running a business and that starts with financial planning.

As a business owner of a beauty salon, managing cash flow, setting budgets, and handling finances are decisions that will require your attention.

But don’t worry, we’re here to guide you through how to understand key financial metrics like the cash flow statement, profit and loss statement, and balance sheet. With a solid financial plan that includes direct costs and advertising expenses, you’ll be well on your way to laying out a comprehensive business plan.

Let’s take a closer look.

Basic financial planning for spas and salons

There are a few key decisions you need to make first when opening a hair salon. Before financial planning begins, you may need to arrange special licenses, and you’ll need to decide on how to hire workers.

You’ll need basic permits and licenses to open your salon. Check your local laws to see what kinds of permits you need, and how often you’ll need to renew them. You may want to consult with an accountant or bookkeeper who works specifically with beauty and wellness businesses in your area to get their recommendations.

You’ll also be hiring workers for your hair salon.

There are two main hiring models to consider:

- Commission-based model: you hire specialists and pay them a percentage of what they bring in.

- Booth rental model: you rent space to specialists, who then act as their own small businesses.

Both models have pros and cons. With an employee model, you have more control over consistency, scheduling, and training. With a rental model, you lose some control, but you reduce costs associated with paying benefits and employment taxes. Of course, each country, region and city will have different employment laws, so be sure to consult with a local expert.

All set up? Let’s talk about creating a solid financial planning strategy to support your salon business for years to come.

Get a handle on your numbers

Good financial planning starts with understanding how your business is doing. Fortunately, today you don’t need to be a bookkeeping whiz – you can use any number of fantastic accounting technology apps that do everything from tracking expenses, taking payments, managing your bookkeeping, and paying bills.

When considering salon accounting software, keep in mind the other apps you use – your scheduling software, POS system, and more. To fully understand your numbers, you’ll want those to be able to integrate. You’ll probably want to consult with your own bookkeeper or accountant to find out what accounting software they recommend (like Xero, QuickBooks, etc.)

Analyze your numbers

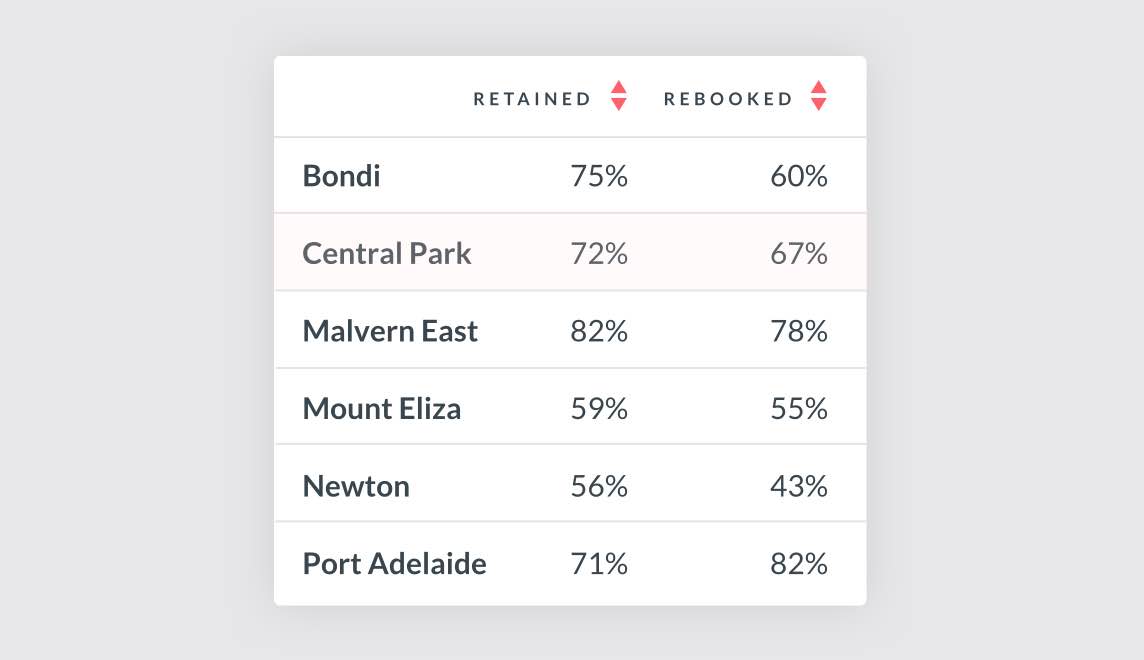

In the past, getting insight into your numbers meant hiring an accountant to analyse your books and write up reports. These days, you can use a salon management software that gives you instant reports on revenue earned, product sales, and other key performance indicators (KPIs).

You need to take an honest look at how your business is doing. That includes knowing how much you’re spending and earning, but also breaking those numbers down in a variety of ways to get the most insight you can. This includes things like revenue by stylist, revenue per appointment, length of appointment, missed appointments, and no-shows, etc.

Questions to ask yourself

- What’s your busiest day of the week?

- What are your best selling products?

- Who are your highest-performing employees?

Answering these questions will help you gain insight into the changes you can make to help your hair salon become even stronger.

Understand your cash flow

One of the big things your financial analysis should show is how much cash you need on hand to keep your business running on a day-to-day basis. Every day, cash comes in from clients. And every day, cash goes out to pay bills, buy supplies, and make payroll. This cycle is your cash flow.

Obviously, a business is doing well when more money is coming in than going out. But there is more to it than that, it’s also a matter of timing. Correctly estimating your cash flow is critical if you want to keep from having nasty surprises like not having enough in the bank account when it comes time to pay rent.

How to get a handle on cash flow

- List out your monthly expenses: rent, utilities, payroll, insurance, purchasing products, loan payments, taxes, and other regular expenses.

- Write down intermittent expenses: equipment purchases, annual training classes, or your yearly holiday party.

- Estimate your monthly income: keep in mind it may vary month-to-month depending on the season.

- Run the numbers: How does your business measure up? If you have more expenses than income, brainstorm ways to trim those and increase your income.

Check in every month to update your cash flow spreadsheet. This helps make sure you’re staying on track, and can spot any red flags before they become a bigger problem.

Quick tip: Don’t forget about gift vouchers! There great way to make some extra cash, but be sure to factor in that you won’t get paid for those services later on.

Resources:

- Xero has a quick tutorial on estimating your cash flow based on past data.

- Or, build your own cash flow spreadsheet with this Microsoft Office template.

Set budgets and goals

Now that you have your expenses, income, and cash flow in hand, it’s time to set your budget and make some goals. With a little bit of creativity, this part can actually be quite fun.

Your budget ensures that your costs stay below your revenue, and allocates monthly spending on things like advertising, salon staff salaries, supplies, and utilities. Most accounting software will have an expense tracking function to help you see how much you spend on things like cleaning supplies and herbal tea in order to set your budget.

Your financial goals should be more than just what you need to stay on budget. They should also help you stretch your business more each month.

Your salon’s financial goals should be more than just what you need to stay on budget. They should also help you stretch your business more each month. By setting your financial goals just a little bit high, you can think of creative ways to meet them.

- What clever way can you fill chairs during your off-peak hours?

- Which add-on services can you offer to boost your average sale?

- What promotions can you plan to bolster the slow season?

Financial planning for the future

The goal of financial planning for your hair salon is to tone down the pressure of the feast-or-famine business. When you understand and analyse your numbers, manage your cash flow, and set budgets and goals, you’ll have a solid foundation to work from.

Don’t get trapped into only thinking about what’s happening today, you need to be thinking about the future, too.

Plan ahead for your seasonal cycles. Many hair salons tend to be busier around the holidays. During peak seasons, sock away the extra cash, during quiet seasons, plan ahead with promotions and events to try to draw in customers.

Use credit wisely

A business credit card can be a good way to smooth out your monthly cash flow, if you commit to paying it off every month. It can also get you in a lot of trouble. Don’t run up debt during the slow season and hope your busy season will earn you enough to pay it off. Managing your credit effectively is a big part of financial planning.

Save, save, save: Set up a savings plan for your future (retirement), and also for bigger business costs like equipment upgrades, taxes, etc. Putting 5-10% of every day’s sales into a savings account for new equipment — or just an emergency fund for a rainy day — will add up without seeming like a big deal at the time. Just be sure to put it somewhere you can’t touch it until you need it.

Start your financial plan with Timely

Timely gives you a window into your business’s financial health. See detailed financial reports on KPIs like staff performance, booking stats, customer spending, product sales, and more. It’s specifically designed to give salons the information they need to make smarter decisions about their businesses.

Your friends might enjoy this

Check out the full guide